Many wealthy individuals share a common mindset: wealth is rarely accidental.

Whether building a retirement fund or setting aside an emergency buffer, financial success grows through deliberate actions, such as monitoring wealth. This approach reflects an internal locus of control, where individuals shape their financial outcomes through data-driven decisions, rather than mere luck.

When tracking net worth, one isn’t simply observing numbers; they are gathering data necessary to make informed decisions, course-correct poor money habits, and identify ways to increase wealth.

Indeed, academic research confirms that monitoring financial wealth is a catalyst for behavioural change. According to findings in the Journal of Economic Psychology, the act of tracking progress toward a financial goal, such as checking bank balances, is likely to adjust their behaviour. This awareness prompts individuals to reduce discretionary spending and make a more significant commitment to long-term savings.

In this light, a wealth monitor functions as a feedback mechanism. It reveals whether financial decisions are working as intended, highlights gaps between goals and reality, and enables timely adjustments before small issues turn into long-term setbacks.

To help you get started, this wealth guide explains how to monitor wealth, from setting financial goals to selecting the right wealth platform to track your net worth.

- Why Monitoring Wealth Matters?

- A Wealth Guide for Beginners: Monitoring Your Wealth Step-by-Step

- Set Financial Goals

- Calculate Net Worth

- Choose the Right Wealth Tracking Tools

- Monitor Wealth Progress

- Analyse Results and Adjust Wealth Strategies Accordingly

- Your Journey to Monitoring Wealth: From Tracking to Thriving

- Track Wealth: Frequently Asked Questions

Why Monitoring Wealth Matters?

Keeping track of wealth gives individuals a clear view of their financial standing. Beyond measuring true financial health, there are other reasons why monitoring wealth is important.

Net Worth Awareness

When monitoring wealth, individuals naturally calculate their net worth, as wealth is determined by the difference between total assets (owned) and liabilities (owed). Net worth, therefore, serves as the key indicator of financial health.

Monitoring wealth, however, goes beyond a one-time calculation. It is the ongoing practice of tracking changes in assets, liabilities, and overall net worth over time.

With increased net worth awareness through a wealth monitor, individuals can:

- Adjust spending, saving or investment strategies to better align with goals.

- Evaluate the impact of debt and develop strategies to reduce liabilities.

- Identify areas of financial inefficiency or unnecessary expenses

- Make informed decisions.

- Plan for major life events, such as buying a first home or building a retirement fund.

To illustrate, upon calculating net worth, an individual might find that their growing credit card debt erodes net wealth, prompting reduced discretionary spending. With this awareness, the numbers are translated into actionable insights that guide smarter financial decisions.

Learn what tells the real financial story: Net Worth vs Credit Score

Financial Goal Tracking

Wealth guide turns broad aspirations into a measurable roadmap. By tracking wealth, individuals can assess how far they are from their goals, which then enables them to identify financial inefficiencies and correct habits that may hinder progress.

For example, after monitoring wealth for four months, an individual realises that monthly dining-out expenses are eroding savings for a planned car purchase. As a result, they adjust their spending and redirect the saved funds toward their down payment.

Risk Management

A wealth monitor also serves as an early warning system, enabling individuals to see how much of their overall net wealth is available before committing significant funds to new investments. This visibility is valuable for investors, as it enables them to manage liquidity risk and ensure they have sufficient resources to cover unexpected expenses or economic downturns without compromising their long-term financial stability.

For instance, an investor considering a large purchase of new bonds might realise, through their wealth monitor, that most of their liquid assets are already tied up in existing traditional investments. With this insight, they can adjust their plan –perhaps delaying the purchase or reallocating cash–so they maintain sufficient liquidity and avoid being forced to sell other holdings at an unfavourable time.

A Wealth Guide for Beginners: Monitoring Your Wealth Step-by-Step

Are you interested in knowing your financial standing? A wealth guide can make this a straightforward process, showing beginners how to calculate net worth, monitor wealth progress, and more.

1. Set Financial Goals

Monitoring wealth begins with clearly defined financial goals. Without a clear target, tracking numbers offer little insight. Financial goals then provide direction and context, helping individuals understand what they are working toward and why their wealth matters.

To set financial goals, it helps to organise them into three categories:

Short-Term Goals

Short-term goals are the "quick wins" of strategic financial planning. While achievable within a day, a month, or even a year, they are vital because they build the discipline needed for larger targets.

Examples of short-term goals include:

- Clearing high-interest credit card debt.

- Set a realistic spending plan and stick with it.

- Saving one month of living expenses.

Medium-Term Goals

Medium-term financial goals, as noted by Smart Asset, form the bridge between short-term priorities and long-term objectives. Generally set for one to five years, they establish a solid foundation and gradually alleviate financial strain over time.

Examples of short-term goals include:

- Establishing and growing diversified investments.

- Purchasing a vehicle.

- Saving for a home down payment.

Long-Term Goals

According to First Financial Bank, long-term goals are strategic objectives designed to solidify your financial foundation, anticipate major future costs, or develop passive income streams. These goals typically span five years or more and centre on milestones such as:

- Becoming debt-free on the primary residence.

- Building a nest egg to maintain lifestyle during retirement.

- Creating assets to transfer to family or future generations.

With goals in place, individuals have clear benchmarks for tracking wealth. By evaluating net worth, cash flow, savings, and investments against these objectives, individuals can see exactly how their plans are progressing.

2. Calculate Net Worth

As mentioned, anyone monitoring their wealth must go through a net worth calculation. But the question remains: how do I find my net worth?

At its simplest, net worth is a snapshot of an individual’s financial health at a specific point in time. It is determined by using the formula:

Total assets (cash + investments + property) – Total liabilities (debts + loans) = Net Worth

To calculate numbers accurately, one must break down their finances into two categories:

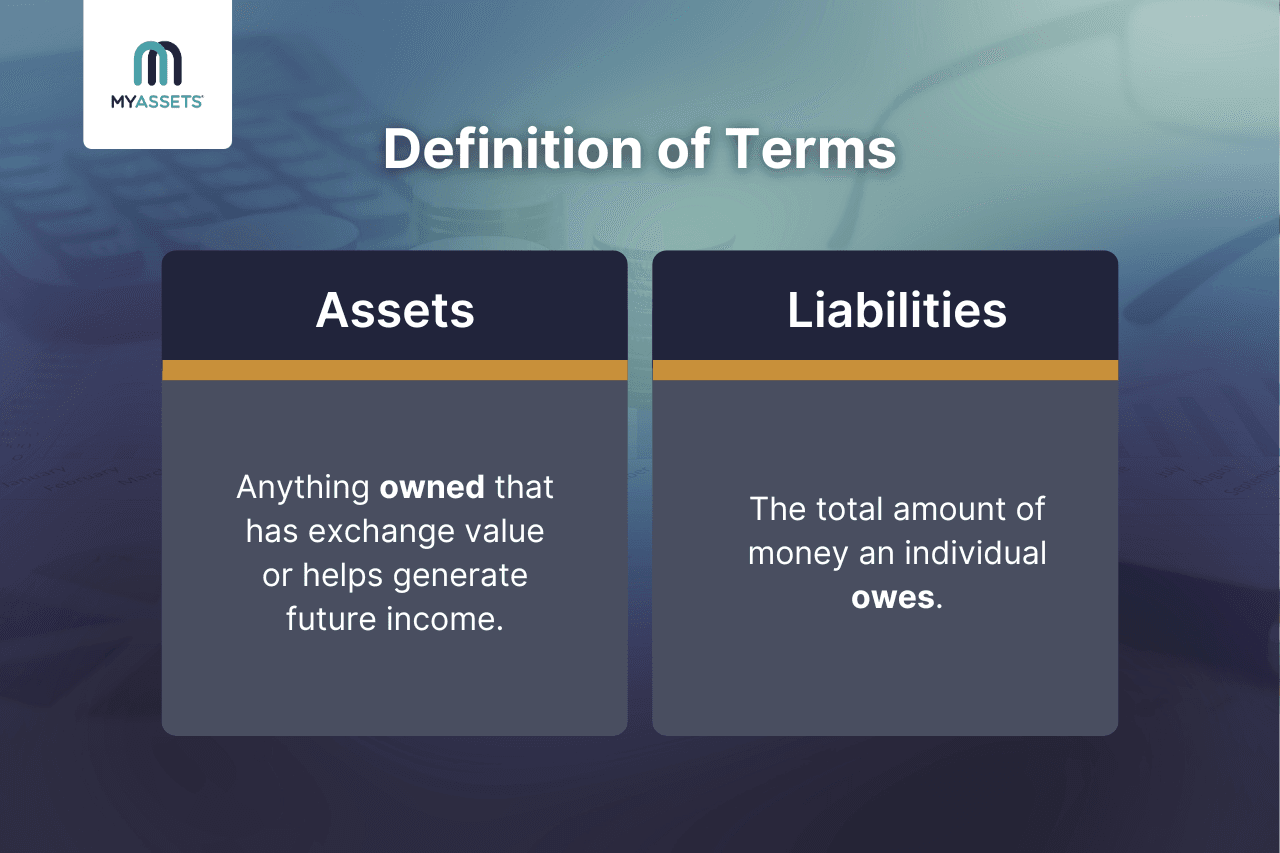

Assets

First, what are assets? As defined by Investopedia, an asset is anything owned that has exchange value or helps generate future income. Essentially, assets are things that store value or generate money, such as:

- Cash and Cash Equivalents

- Checking Accounts

- Physical Cash

- Savings Accounts

- Investments

- Bonds

- Cryptocurrency

- Exchange-Traded Funds (ETFs)

- Mutual Funds

- Retirement Accounts, i.e., 401(k)

- Stocks

- Real Estate

- Land

- Primary Residence

- Rental Properties

- Vacation Homes

- Personal Property

- Artwork and other collectable Investments

- Electronics and Appliances

- Jewellery

- Vehicles (cars, boats, motorcycles)

- Watches

- Luxury Items

Liabilties

In contrast, liabilities represent the total amount of money an individual owes. These are financial obligations that remain unpaid or outstanding and can be classified as:

- Auto Loans

- Credit Card Debt

- Medical Bills

- Mortgage

- Outstanding Insurance Premiums

- Personal Loans

- Student Loans

- Taxes Owed

- Utility Bills

Once all assets and liabilities are listed with their corresponding values, individuals can calculate net worth using the standard formula: total assets minus total liabilities.

Remember, a positive net worth shows that assets surpass liabilities, reflecting strong financial health and stability. Conversely, a negative net worth, where liabilities exceed assets, highlights potential financial challenges, according to Farmers State Bank.

3. Choose the Right Wealth Tracking Tools

For individuals monitoring net worth, using a wealth tracker is highly recommended. These wealth management solutions offer a comprehensive view of one’s financial landscape by consolidating all assets and liabilities in one platform.

This naturally raises the question: which wealth tracker is right for you?

Two of the most popular methods are spreadsheets and wealth apps. To determine which option best fits your needs, it helps to understand the key differences between them:

| Category | Wealth Tracking Spreadsheet | Wealth Tracking Software |

|---|---|---|

| Definition of Terms | A tool that arranges data in rows and columns to help users manage, calculate and analyse data. | A platform that consolidates and calculates an individual’s entire financial portfolio into a single dashboard. |

| Best For | Those who want total control, high customisation, and no subscription fees. | Users looking for automation, ease of use, and quick, on-the-go access. |

| Primary Features | - Custom formula creation - Manual data entry cells - Static charts and tables |

- Automated financial calculation - Bank syncing - Interactive charts and tables |

| Customisation | Fully customisable categories, formulas, layouts, and reporting. | Limited to predefined categories and dashboards. |

| Ease of Use | Requires knowledge of spreadsheet functions; setup and maintenance can be time-consuming. | User-friendly and intuitive interfaces; easy to moderate setup required. |

| Automation and Insights | Limited; charts and analyses must be manually built. | Built-in charts, dashboards, alerts, and insights for net worth. |

| Cost | Free or one-time fee for templates; no ongoing subscription. | Typically offers a free basic version; premium features may require a monthly or annual subscription. |

In summary, those who value flexibility and control often find spreadsheets to be the ideal choice, allowing for full customisation and hands-on management. Wealth tracking apps, on the other hand, emphasise automation and convenience, making them well-suited for individuals who prefer real-time updates, goal tracking, and a simplified approach to monitoring their finances.

Ultimately, selecting the best wealth tracker is a highly personal decision, as individuals approach wealth planning in different ways.

![]()

4. Monitor Wealth Progress

Monitoring progress is the ongoing tracking of financial metrics to see how wealth is changing over time. It is where individuals move beyond wealth planning and actively observe what is happening without making changes immediately.

To monitor progress, these metrics provide valuable insight:

Net Worth

Net worth is a crucial metric that measures the relationship between assets and liabilities, indicating whether overall wealth is growing or declining over time.

When data reflects a consistent upward trend, it signals positive wealth growth, validating that current financial habits are effective. Conversely, a stagnant or declining trend acts as an early warning sign, indicating the need to reassess and adjust financial decisions.

Discover apps to track your wealth: 10 Best Net Worth Tracker Apps

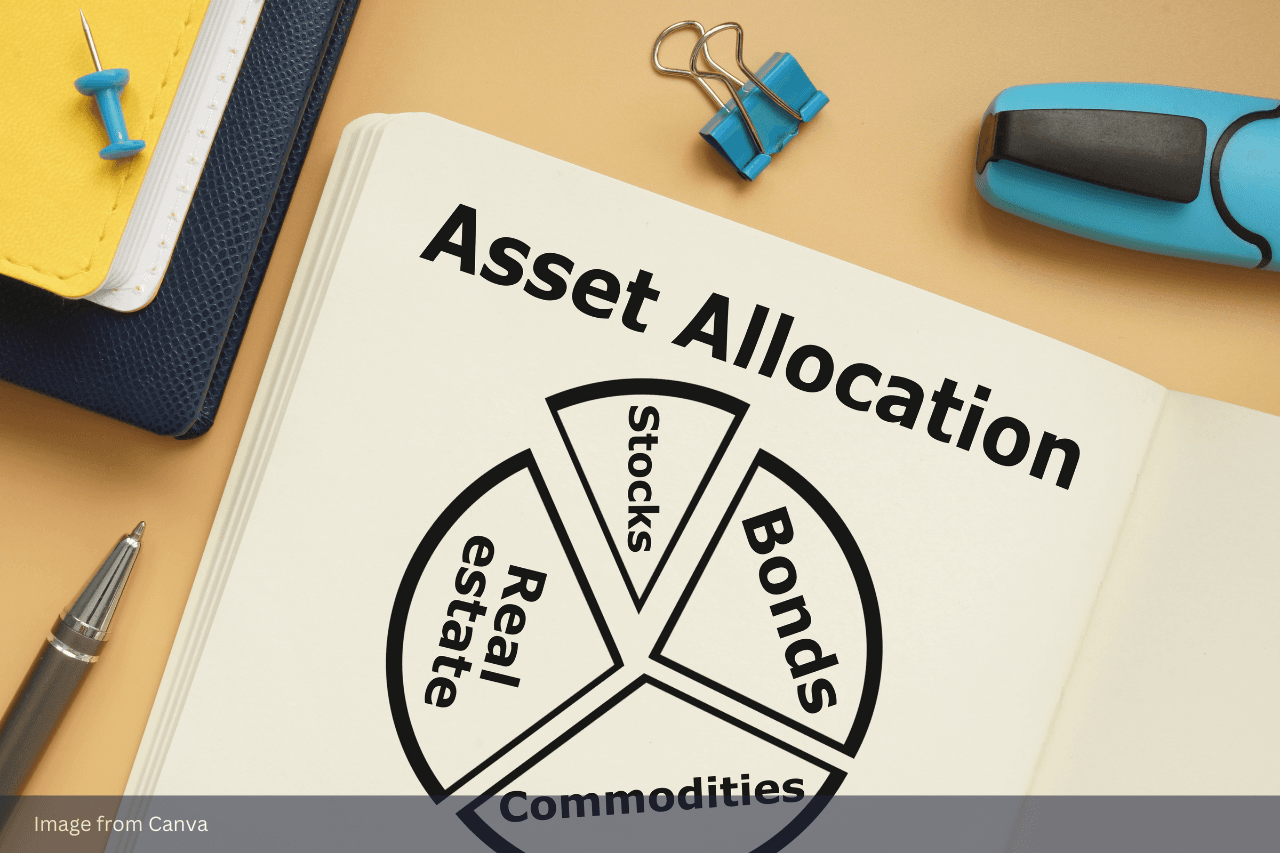

Asset Allocation

Asset allocation refers to the distribution of wealth across various asset types, including cash, investments, property, and alternative assets.

Regularly monitoring this distribution helps identify concentration risks and imbalances, ensuring that no single asset class dominates the portfolio.

Cash Flow

Cash flow is a critical financial metric that tracks the movement of money into (inflow) and out of (outflow) an individual’s finances.

It provides insight into how financial inflows (rental income, dividends, capital gains) and outflows (utility bills, rent payments, credit card bills) affect day-to-day financial health.

Results translate into the following:

- Positive cash flow occurs when inflows consistently exceed outflows, creating a surplus that can support saving, investing, and long-term financial goals.

- Negative cash flow happens when outflows surpass inflows, signalling that spending may be outpacing earnings. This highlights the need to review budgets, reduce unnecessary expenses, or adjust financial strategies.

Read more: Best Cash Management Solution: A Complete Guide

5. Analyse Results and Adjust Wealth Strategies Accordingly

Analysing results involves reviewing tracked wealth data to make informed decisions. Monitoring wealth is not a passive act of observation; it is a feedback loop designed to trigger action.

That said, this phase involves stepping back from day-to-day numbers and asking relevant questions, such as:

- Are short, medium, and long-term goals being met as planned, or has the timeline shifted?

- Are there any unexpected changes in income, expenses, or market conditions that require adjustment?

- Does the current asset allocation still reflect the individual's actual risk tolerance and time horizon?

- Does the current financial standing align with the goals set at the beginning?

- Have there been any changes in income, expenses, or the market that require action?

Once the assessment is complete, strategies can be adjusted to:

- Keep wealth strategy intentional, relevant and resilient.

- Respond proactively to financial or life changes.

- Stay aligned with personal goals.

Your Journey to Monitoring Wealth: From Tracking to Thriving

Monitoring wealth is about gaining clarity, direction, and control over financial decisions. Rather than viewing finances in isolation, it provides a structured way to see how all financial elements work together and contribute to overall progress.

This step-by-step wealth guide shows that wealth monitoring is a continuous cycle: setting goals, tracking progress, analysing results, and adjusting strategies as circumstances change. When done consistently, it transforms financial data into insight and insight into action.

Ultimately, a wealth monitor helps beginners move beyond passive observation by:

- Ensuring long-term goal alignment.

- Strengthening financial discipline.

- Supporting intentional decision-making.

All of which lay a solid foundation for sustainable wealth growth.

Track Wealth: Frequently Asked Questions

1. What is the best way to track wealth?

The best way to track wealth is by using wealth platforms that give a complete overview of finances. Spreadsheets offer flexibility, while wealth tracking apps like MyAssets provide automation and convenience. Choice depends on personal preference and style.

2. What are common wealth tracking mistakes?

Monitoring net worth irregularly reduces its usefulness. Without frequent updates, identifying trends or taking timely financial action becomes difficult. Reviewing finances only occasionally, once or twice a year, makes it challenging to accurately measure progress.

3. What is the 70/20/10 rule money?

The 70/20/10 rule is a budgeting method in which 70% of income is used for everyday expenses, 20% is dedicated to financial goals like savings or investments, and 10% is set aside for debt repayment or charitable contributions.

MyAssets: The Ultimate All-in-One Wealth Tracker

Do you monitor your wealth? Managing finances without visibility is like navigating without a map. Wealth tracking tools such as MyAssets provide the clarity needed to stay on course.

Designed to organise, track, and manage assets, MyAssets gives users a full 360-degree view of their wealth by consolidating information from all accounts in one place.

One Dashboard for All Your Wealth

It pulls in everything —from bank accounts (checking and savings), investment portfolios (stocks, bonds, and mutual funds), and properties (residential, rental, and commercial), to valuable assets like family heirlooms, collectable investments, and everyday belongings.

It gets better. MyAssets doesn’t just show one’s assets; it also incorporates their liabilities, such as:

- Credit card debts

- Loans

- Mortgages

Imagine having all this information presented in a visually appealing dashboard. With MyAssets, monitoring wealth becomes straightforward as the platform transforms raw numbers into dynamic charts, offering a breakdown of how resources are distributed across finances, properties, collectables, and even belongings.

Secure Shared Access to Your Wealth

Are you tracking your wealth with the help of others? Managing wealth is rarely a solitary endeavour, yet sharing sensitive financial data often poses a significant security risk. MyAssets addresses this by providing individuals with full control over account permissions, with the Delegates feature allowing them to assign who can view, edit, delete, or create entries within their portfolio.

This granular control enables seamless collaboration without compromising total privacy. For example, an individual can grant:

- View-Only Access to a financial advisor to monitor investment performance and provide strategic guidance.

- Edit Permissions to a spouse or partner to ensure household assets and shared liabilities are updated in real-time.

In this way, MyAssets ensures that data remains protected when managing sensitive information with others.

Track every asset, grow your wealth with MyAssets, free for 14 days.