It is a common misconception that having a perfect credit score guarantees a high net worth or that owning significant assets automatically translates to a high credit score.

In fact, CNBC emphasises that individuals can have an excellent credit score and still carry a negative net worth, or conversely, hold significant wealth yet carry the lowest credit score. This raises a critical question: Which of these tells the story of an individual's financial health?

While a credit score reflects how reliably someone manages borrowed money, calculating net worth, on the other hand, reveals the full picture of what they own versus what they owe.

These two financial indicators might seem unrelated at first glance, but they often work in tandem, each significantly impacting a person's overall financial standing.

Ultimately, understanding the difference between net worth and credit score can be tricky, but this article makes it easy. By the end, readers will be able to identify what credit score and net worth mean, when each matters, and how they influence one another to shape financial insight and achieve personal financial success.

- Net Worth vs. Credit Score: Understanding Their Roles in Financial Health

- How Net Worth and Credit Score Impact Each Other

- Paying Off Debt Improves Net Worth and Credit Score

- Missed Payments Damage Credit, With Net Worth Effects Later

- Using Credit to Build Assets

- Net Worth and Credit Score: The Two Pillars of Financial Growth

- Net Worth vs Credit Score: Frequently Asked Questions

Net Worth vs. Credit Score: Understanding Their Roles in Financial Health

Net worth and credit score are often used to gauge financial well-being, but they reflect different aspects of a person’s finances. This article breaks down their differences by explaining what each measures, the insights they offer, and when they matter most in various cases.

Defining Net Worth and Credit Score

To fully understand what each term means, this article breaks down their definitions.

What is Net Worth?

The Corporate Finance Institute defines net worth as an individual's total financial value, calculated by subtracting their liabilities (what they owe) from their assets (what they own). In simpler terms, it is the result of:

Net Worth = Assets − Liabilities

What is a Credit Score?

A credit score, as defined by Equifax, is used by lenders to evaluate whether an applicant qualifies for financial products, such as credit cards, loans, mortgages, or other services.

Additionally, lenders evaluate an applicant's creditworthiness by using a numerical score generated from a mathematical model. This score comes directly from the individual's credit report, which serves as a detailed summary of their credit history, encompassing records like:

- Balances Due

- Credit Accounts

- Credit Limits

- Payment History Details

Not only that, Lloyds Bank emphasises that affordability is also considered when calculating a credit score. Lenders review an applicant’s capacity to repay by examining the following:

- Employment Status

- Existing Borrowing

- Income

- Regular Expenses

What Do They Reveal?

In the world of personal finance, understanding financial standing is crucial. Two key metrics often come into play: net worth and credit score. But what do these two metrics really say about one's financial health? This article breaks down the insights each offers.

Financial Insights of a Net Worth

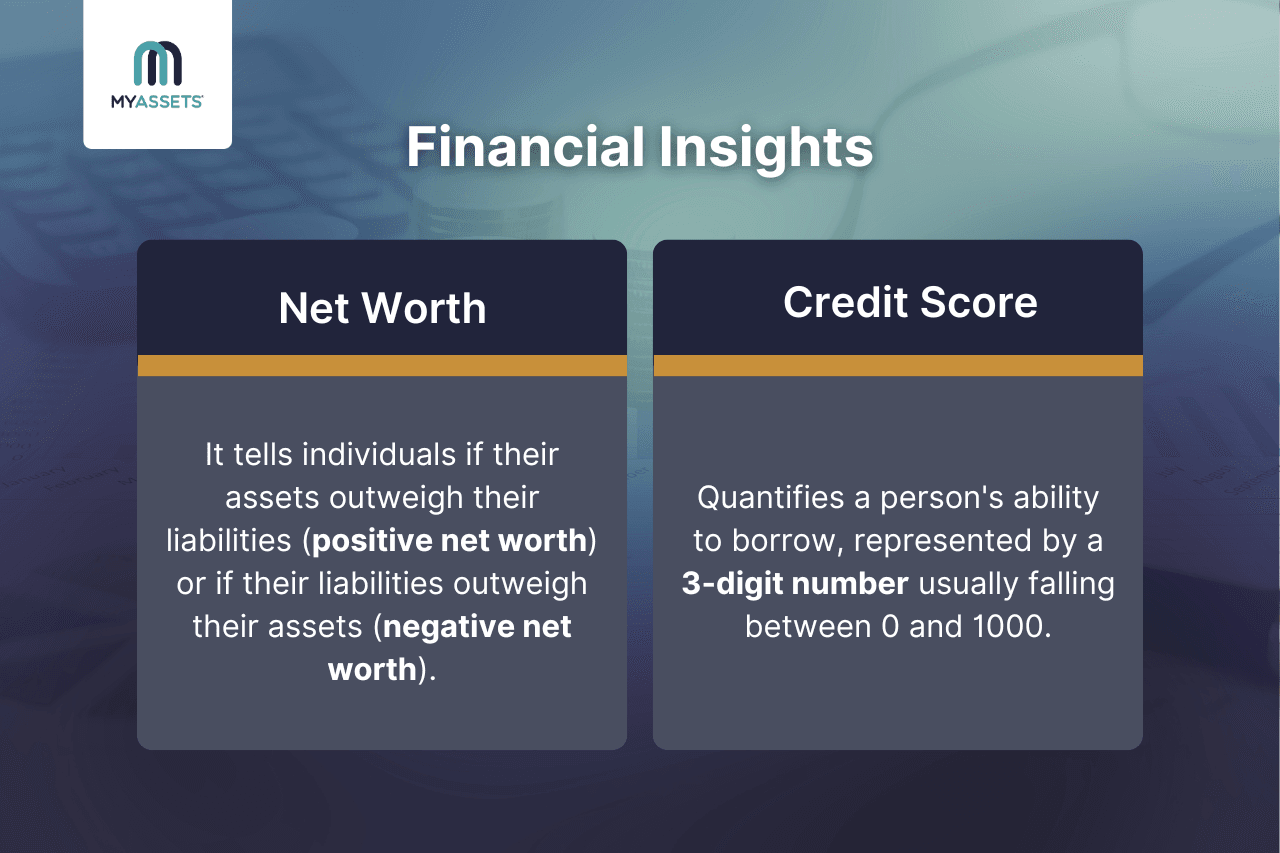

Net wealth calculation shows individuals their overall financial position by providing two results:

(1) a positive net worth, which means a person owns more than what they owe.

Indeed, Investopedia notes that a consistently positive and growing net worth signals strong financial health. This steady increase suggests that an individual is effectively building wealth by growing their assets—such as income, savings, and investments—while also actively reducing their debts.

Conversely, (2) a negative net worth means an individual owes more than what they own, indicating liabilities outweighing their assets.

While a negative net worth indicates high debt, it can also signify a temporary state, says Yahoo Finance. Take the case where an individual has recently taken on a substantial mortgage, leading their immediate liabilities to exceed their current total assets.

However, as the property gains value over time and they diligently pay down their mortgage, their net worth is expected to recover and, ideally, grow significantly.

Ultimately, regardless of whether an individual’s net worth is positive or negative, this indicator serves to measure progress toward financial goals, simultaneously revealing the extent to which current assets can withstand unforeseen fiscal shocks.

See Also: 5 Powerful Strategies to Increase Your Net Worth

Financial Insights of a Credit Score

So, what does my credit score say about my overall financial health? Essentially, the credit score indicates an individual’s borrowing behaviour and the likelihood of them responsibly managing their repayments.

In the UK, credit scores are provided by three major UK credit bureaus—Experian, Equifax, and TransUnion—each using its own grading scale. The table below outlines what is considered a good credit score with each agency.

a. Experian UK Credit Score

| Excellent | Good | Fair | Poor | Very Poor |

|---|---|---|---|---|

| 961 - 999 | 881 - 960 | 721 - 880 | 561 - 720 | 0 - 560 |

b. Equifax UK Credit Score

| Excellent | Very Good | Good | Fair | Poor |

|---|---|---|---|---|

| 811 - 1000 | 671 - 810 | 531 - 670 | 439 - 530 | 0 - 438 |

c. TransUnion UK Credit Score

| Excellent | Good | Fair | Poor | Very Poor |

|---|---|---|---|---|

| 628 - 710 | 604 - 627 | 566 - 603 | 551 - 565 | 0 - 550 |

Generally, possessing a higher credit score provides several benefits. This includes improving the chances of loan and credit application approval, allowing for the attainment of lower interest rates, and often results in more generous credit limits.

Contrarily, a poor credit score can negatively impact borrowing, leading to higher interest rates, limited financial products, and potential loan rejections. This highlights the relevance of maintaining a good credit score to access more favourable financial opportunities.

When Do They Matter Most?

There are specific life moments and financial decisions where net worth and credit score become critical. But the question here is: When do they truly take centre stage, and why?

This article clarifies when each matters most, facilitating readers' familiarisation with the roles of these metrics in different financial situations.

Situations Where Net Worth is Vital

There are stages where net worth plays a significant role, as it primarily provides a snapshot of one’s financial position.

Below are some situations where net worth is notably useful for decision-making and long-term planning.

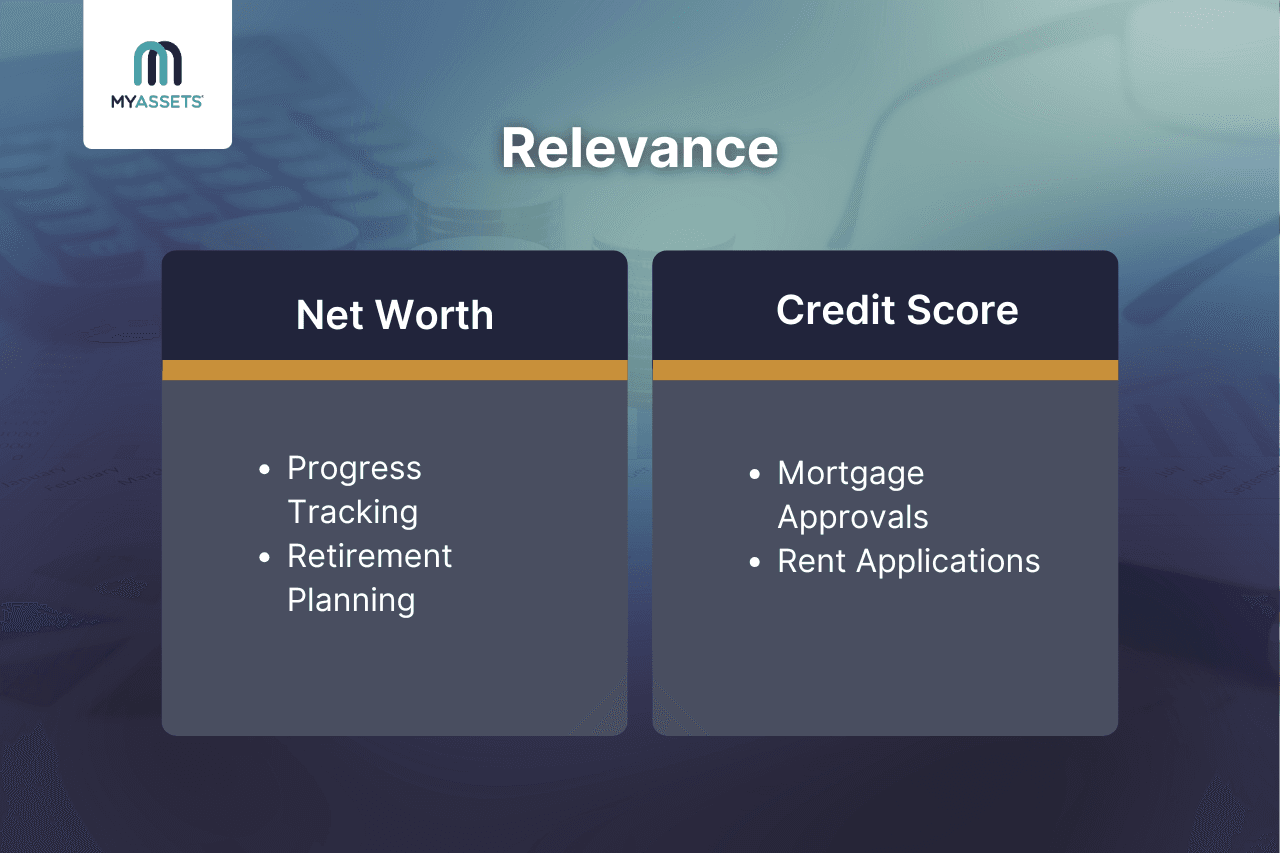

Progress Tracking

Monitoring one's net worth allows individuals to effectively track their progress toward various financial goals, as noted by the United States Senate Federal Credit Union.

Whether the aim is a comfortable retirement, homeownership, or significant debt reduction, net worth provides a clear snapshot, helping individuals assess if they are on the right track and enabling them to make necessary adjustments to their financial strategies.

Retirement Planning

Upon retirement, individuals generally stop earning employment income, yet their living expenses—including utilities, groceries, healthcare, and transportation—continue, as highlighted by AOL.com.

In this case, net worth is vital in determining whether an individual has sufficient resources to sustain their desired lifestyle in retirement. Whether drawing from retirement accounts, investment income, or proceeds from asset sales, net worth serves as a guiding measure for aligning retirement goals with available financial resources.

Beyond this, net worth is equally vital for estate planning, as it offers a comprehensive understanding of their accumulated assets and liabilities. This insight helps identify transferable assets, making it easier to plan and execute an efficient asset transfer to beneficiaries.

Read More: Net Worth for Retirees: How to Retire Comfortably in the UK

Financial Events Where Credit Score is Crucial

A credit score serves as a reliable indicator of repayment behaviour, making it a key factor in accessing financial opportunities. To learn more about credit scores, this article explores credit-related events that demonstrate why a good credit score matters.

Mortgage Approvals

When taking a loan to purchase a house, it is the applicant’s credit history which influences the mortgage interest rate offered, as lenders assess risk and eligibility based on past borrowing behaviour.

According to a UK credit bureau, Equifax, the range of available mortgage products—including special introductory rates or other favourable terms—is often limited. These offers are typically reserved for applicants whose credit history demonstrates a consistent pattern of responsible borrowing and meets specific standards set by the lender.

Fundamentally, a strong credit history is the cornerstone of a high credit score. This favourable score is vital in the mortgage application process as it opens the door to better mortgage options and lower long-term costs for a home loan.

Rent Applications

When submitting rental applications, landlords often examine an individual's credit score to assess the tenant's capability to pay rent in full and on time.

According to an estate agent, Cope & Co., there are primary reasons why a credit score matters when renting a property in the UK:

- Deposits and Guarantors: Individuals with lower credit scores may face requests for higher deposits or the need for a guarantor, as landlords perceive them as a greater risk.

- Rental Terms: A good credit score can lead to more favourable rental terms, potentially giving tenants greater negotiating power for aspects like a longer lease or even reduced rent.

- Tenancy Approval: A high credit score increases the likelihood of tenancy approval, as landlords view it as a strong indicator of timely rent payments.

Essentially, checking credit scores through a UK credit bureau (i.e. Experian, TransUnion, and Equifax) is significant for understanding financing prospects. This practice enables individuals to proactively monitor their financial standing and implement techniques in case they need to improve their credit score.

How Net Worth and Credit Score Impact Each Other

While often discussed separately, net worth and credit score are two crucial metrics that can significantly influence each other. So, how exactly do they impact each other, and what does that mean for your financial health?

This article explains the relationship of these metrics and their collaborative impact on one’s financial well-being.

Paying Off Debt Improves Net Worth and Credit Score

While paying off debt improves net worth by reducing liabilities, lowering credit card balances and fully settling loans on time, on the other hand, can also boost one's credit score.

This practice demonstrates a positive effect on net worth and credit score as it signals responsible personal finance management to lenders. Simultaneously, lowering debts results in freed-up money that can then be used for saving or investing, further enhancing financial health, said Credit Sesame.

Missed Payments Damage Credit, With Net Worth Effects Later

A credit score is primarily the result of an individual's debt repayment behaviour. Thus, if one misses a payment, it directly and negatively affects one's credit score.

This naturally leads to the question: How does this affect net worth? To answer this, late payments can incur significant costs, such as late payment charges and penalty interest rates, which add to one's liabilities.

Over time, these added costs can gradually diminish an individual's financial reserves, reducing the value of their assets relative to their debts and thus negatively impacting their overall net worth.

Using Credit to Build Assets

Leveraging borrowed money to acquire an asset that would potentially increase in value or generate income over time is a concept called good debt.

The following examples illustrate how credit can be used strategically:

- Business Loans: Provide essential capital for ventures designed to generate income and grow in value.

- Education Loans: Represent an investment in human capital, leading to enhanced skills and a higher earning potential over a lifetime.

- Mortgage: Facilitate the acquisition of real estate, an asset that typically appreciates and builds equity over time.

While these types of credit are indeed forms of debt, they are considered good debt as they facilitate the acquisition of assets that can generate long-term financial returns and enhance an individual's net worth.

Net Worth and Credit Score: The Two Pillars of Financial Growth

While both net worth and credit score are critical indicators of financial health, they tell distinct yet interconnected stories.

Net worth offers a holistic view of an individual's financial standing by summarising all assets versus liabilities, painting a picture of overall wealth and long-term financial security. Credit score, on the other hand, provides an assessment of one's reliability as a borrower, influencing access to and the cost of credit.

Crucially, these two financial metrics share a reciprocal relationship. Responsible credit management can boost an individual's credit score, which in turn often unlocks better loan terms. These more favourable terms reduce borrowing costs, effectively freeing up capital. This freed-up capital can then be allocated towards building assets, ultimately leading to net worth growth.

In this context, net worth and credit score are two separate metrics that create a powerful domino effect. When managed strategically, an improvement in one can trigger a positive chain reaction in the other, leading to overall financial betterment.

Net Worth vs Credit Score: Frequently Asked Questions

1. What is the difference between net worth and credit score?

Net worth measures an individual’s overall financial position by subtracting total liabilities from total assets. In contrast, a credit score reflects their creditworthiness based on borrowing and repayment history.

2. Does having a high net worth mean I’ll have a good credit score?

Having a high net worth does not guarantee a strong credit score. While net worth measures overall financial position, credit scores assess how one manages debt. However, when both are managed strategically, strengthening one can positively influence the other.

3. Which tools or apps are best for tracking net worth in the UK?

Net worth tracking apps like MyAssets, Empower, and Kubera consolidate financial data—accounting for assets and liabilities—to give users a clear view of their net worth.

Your Real Financial Picture, Revealed by MyAssets

Every financial journey tells a unique story, and understanding it requires a complete picture. MyAssets helps users reveal that story, showing them their real financial position through their net worth.

MyAssets is a net worth tracker app. It provides users with a complete understanding of their financial standing by allowing them to easily add all their financial accounts—from cash and bank accounts to investments, insurance policies, and properties—to see a detailed breakdown of their assets in one convenient place.

As a net worth calculator app, MyAssets lets users include credit card balances, loans, and mortgages to ensure liabilities are fully accounted for. What sets MyAssets apart is its ability to link each debt to its related asset—associating a mortgage account with the property it finances, giving users a clear view of what is owed and where it stands.

Interested to know more? Discover the real story of your finances with MyAssets’ 14-day free trial.