Ever imagined owning a slice of paradise–perhaps a beachfront bungalow in Brazil, a rustic farmhouse in France, or a sunlit villa in Greece?

For many, the allure of buying property abroad is undeniable, promising not just a wall and a roof but an entirely fresh lifestyle.

What feels like an escape in imagination is a lived experience for many. According to research from Wise, over 1.5 million British citizens have already purchased properties overseas, a testament to the popularity of international real estate.

From property investment ambitions to leisure escapes and retirement plans, the motivations behind are as diverse as the destinations themselves. However, regardless of the reason, the process of purchasing property overseas is a world away from doing so at home. Learning how to buy overseas property requires a careful understanding of the unique rules, regulations, and potential pitfalls.

Luckily, this article explains everything you need to know about buying overseas property, from its benefits to seven crucial tips before you buy.

- Why Buy Properties Overseas?

- 7 Things to Know Before You Purchase Property Abroad

- Local Property Market Drivers

- Limitations of Overseas Property Ownership

- Local Taxes Applying to Property Owned Abroad

- Financing Options for Foreign Real Estate Buyers

- Title Deed for Property Owners

- Buying Property and Residency Rights

- Digital Tools for Overseas Property Oversight

- Is it Worth Owning Property Abroad?

- Buying Overseas Property: Frequently Asked Questions

Why Buy Properties Overseas?

For many, buying property abroad is as much about fulfilling lifestyle ambitions as it is about making a sound investment. This article reveals the most compelling reasons why people explore international real estate.

Lifestyle Benefits

One of the benefits of owning overseas real estate for property owners is the freedom to choose an ideal environment, whether they seek a slower, more relaxed pace of life or the vibrant energy of a bustling city.

Take Portugal, for instance: its Mediterranean climate and laid-back charm make it a favourite for those dreaming of a European escape. Meanwhile, retirees often gravitate toward Panama, a country that boasts one of the best healthcare systems, according to Forbes.

With such a diverse range of destinations, buying a house abroad that perfectly matches one’s lifestyle goals and personal priorities has never been more attainable.

Financial Incentives

Beyond personal benefits, purchasing a property abroad offers a compelling set of financial incentives that can contribute to an increase in net worth.

To be more specific, an overseas property can serve as a crucial hedge against localised risks. Meaning that despite political instability or economic downturns affecting domestic property values, the foreign property investment may retain or even increase its value during such periods, says property platform Properstar. This geographical diversification then protects and strengthens a portfolio against unexpected volatility in one’s home country.

Additionally, renting out a property overseas can serve as a dependable income strategy for those seeking opportunities beyond domestic borders. Whether offering short-term stays in a beachfront villa or a long-term lease in a bustling city, property investors can generate a steady cash flow. This is especially lucrative in markets with a high influx of tourists or strong demand from expatriates and professionals willing to pay for comfortable accommodations.

Read More: What Is Property Portfolio Management?

7 Things to Know Before You Purchase Property Abroad

The idea of finding properties abroad to buy often conjures images of Mediterranean villas, chic city apartments, or serene country homes. But behind the appeal lies a process which includes economic, legal, and financial challenges. This article breaks down what you need to know to make your purchase with confidence.

1. Local Property Market Drivers

Spot Blue, a real estate agency, emphasises the relevance of understanding the local market. Buyers need to analyse average property prices and track key market trends to ensure fair value.

Foreign investors looking at the local market should focus on the following key areas:

- Comparable Sales: Review recent transactions of similar properties within the area to gauge market value.

- Demographic Shifts: Analyse changes in population characteristics such as age distribution, income levels, and migration trends.

- Economic Factors: Track local economic conditions through indicators like employment rates, job growth, and prevailing interest rates.

- Neighbourhood Amenities: Consider the influence of schools, public transportation, infrastructure developments, and other community features on property prices.

- Supply and Demand: Measure the balance between available listings and buyer interest to understand pricing pressure.

Ultimately, understanding these market drivers is crucial for finding the right property abroad and making a sound investment.

2. Limitations of Overseas Property Ownership

As strongly recommended by gov.uk, aspiring buyers must research and comply with the local laws regarding property acquisition and rental overseas, as each nation has a distinct legal framework for foreign ownership.

A clear example of this can be observed in Thailand. Foreign nationals can legally acquire condominium units, but there is a strict quota: foreign ownership within a single condominium building cannot exceed 49% of the total sellable area. According to legal expert Siam Legal, the remaining 51% must be owned by Thai nationals, a point foreign investors must verify before committing to a purchase

These rules exist to protect a nation's interests, regulate land use, and maintain a stable property market. Therefore, it is imperative for foreign investors to hire professional legal counsel to help them navigate these complex regulations and ensure a smooth, legal transaction.

3. Local Taxes Applying to Property Owned Abroad

Owning a property overseas comes with a range of ongoing financial obligations that significantly impact the total investment cost. This raises an important question: What recurring costs should one be prepared for?

To begin with, owning property abroad means paying property taxes. These taxes, according to property-buying resource Your Overseas Home, differ significantly based on the country of purchase. Here are some examples from well-known overseas markets:

- Greece: Imposes a 3.09% tax on property purchases. Additionally, a 15% tax is applied to capital gains from property sales. Rental income is taxed at a rate ranging from 15% to 45%, as highlighted by Global Citizen Solutions.

- Italy: Non-residents or those purchasing a second home are subject to an additional 9% tax on the property's cadastral value, in addition to the standard Italian property tax, known as Imposta Municipale Unica (IMU).

- Portugal: Individuals are subject to an annual property tax called Imposto Municipal sobre Imóveis (IMI), which functions similarly to the UK's council tax. The tax rate, which ranges from 0.3% to 0.8%, is determined by the property's type, location, and age.

Given that tax rules are subject to change and often include exemptions or varying rates, enquiring for expert advice is highly recommended.

Moreover, beyond property taxes, there are several other recurring costs that owners should factor into their budget:

- Insurance: A crucial expense to protect investment against damage, natural disasters, theft, or other unforeseen events.

- Maintenance and Repair Costs: Routine upkeep and unexpected repair costs, such as pest control, cleaning drains, repairing windows, and repainting –all of which are inherent in older properties.

- Management Fees: If renting out property or will not be living there full-time, a property manager is often necessary, and fees typically range from 8% to 20% of the rental income.

- Utility Bills: Includes essential services like electricity, water, gas, internet, and phone.

In essence, factoring in these costs helps foreign property owners stay aware of their financial obligations, ensuring they don't overpay due to non-compliance.

4. Financing Options for Foreign Property Buyers

When it comes to purchasing overseas property, one of the most significant costs a person will face is securing a mortgage. A mortgage represents a substantial financial commitment, making it relevant to understand how it works when buying property in a different country.

An overseas mortgage is a loan specifically for a property located outside a person’s country of residence, as defined by the non-profit consumer organisation, Which?. For example, a person living in the United Kingdom who wishes to buy a vacation home in Spain would need to apply for an overseas mortgage.

According to Wise, obtaining this type of loan is likened to getting a mortgage for a property in one's home country. However, the applicant has two options when securing the loan:

- UK-Based Provider: They can apply for a specialised overseas mortgage product from a UK-based provider, such as HSBC’s international mortgage.

- Foreign Bank: They can apply directly to a foreign bank or lender in the country where the property is located. For instance, BNP Paribas offers mortgages for non-residents looking to buy a home in France.

In either case, the applicant must meet standard eligibility and income requirements and provide supporting documents, just as they would for a domestic mortgage. However, depending on the country, they may encounter additional steps when applying for mortgage for property abroad.

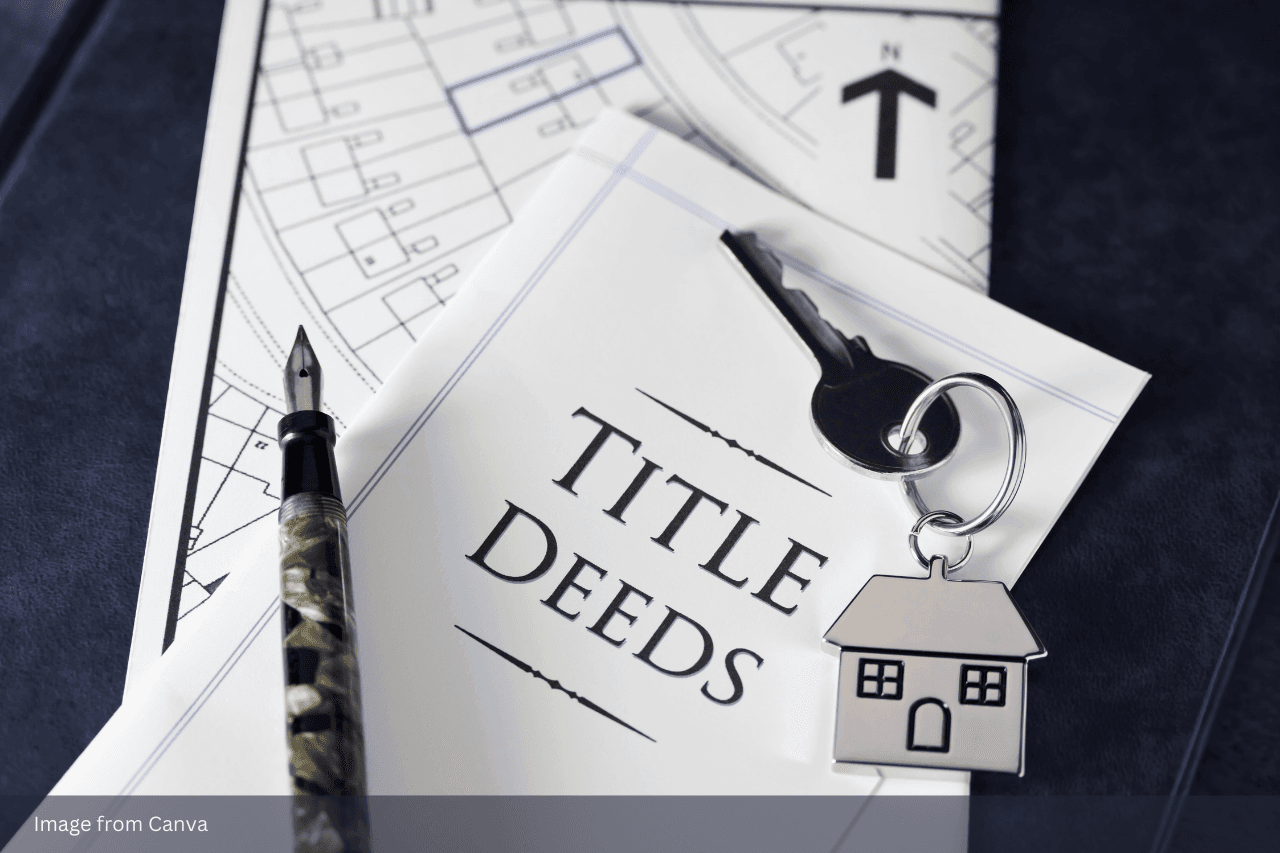

5. Title Deed for Property Owners

Before anything else, what are title deeds? Gov.uk defines these as legal documents that prove the chain of ownership for a piece of land or property. They act as a historical record, showing every person who has owned the property and the details of each transfer.

The follow-up question here is: why is a title deed so important?

It is because title deeds offer protection against common legal issues, such as:

- Property Rights Dispute: A recognised title deed prevents future claims or disputes over who owns the property. Lack of such a document could lead to lengthy and costly legal disputes if a former owner or their heirs contest possession.

- Fraudulent Sales: A title deed confirms purchase of property overseas from its rightful owner. It safeguards individuals from scams where someone tries to sell a property they don't legally own.

- Unexpected Debts or Liens: The title deeds disclose any existing financial burdens on the property, such as mortgages or legal liens. This prevents one from unknowingly inheriting the previous owner's debts.

A clear title deed is the best protection for an individual's property purchase abroad. It not only confirms they are the rightful owner but also safeguards them from financial risks and legal disputes that could arise after their purchase.

6. Buying Property and Residency Rights

Tekce emphasises that property ownership does not always grant a person the right to live in a country long-term, but it is recognised as a qualifying factor for residency in some countries.

This is where programs like a Golden Visa come into play. Unlike a standard residency permit based on a person's purpose for being in the country (i.e., employment or study), a Golden Visa is designed to attract foreign investment.

What is a Golden Visa?

As noted by Investopedia, a Golden Visa offers a pathway to long-term residency in exchange for a substantial financial investment, through real estate, business development, a bank deposit, government bonds, and investment funds.

Which countries have a Golden Visa?

According to Henley & Partners, the countries most recognised for offering these programs include:

- Australia

- Canada

- Cyprus

- Greece

- Italy

- Malta

- New Zealand

- Portugal

- Spain

- United Arab Emirates

Ultimately, while a Golden Visa provides a fast-track to residency, it is a path only viable for individuals who can manage substantial financial investment required by such a program.

For those with a limited budget, a standard residency permit is a traditional alternative to a Golden Visa. While the process is often more complex, with a longer processing time and stricter residency requirements, being well-informed of these options helps individuals plan their stay and comply with local immigration laws.

7. Digital Tools for Overseas Property Oversight

While managing a property portfolio is no small task, handling it from across the globe presents greater challenges. Fortunately, the digital age has made this process more manageable.

By leveraging various property management apps and software, property owners can remotely oversee all aspects of their properties. These tools streamline and automate key processes, from managing finances and finding tenants to handling maintenance issues, all without the need for physical presence.

Highlighted below are some notable property management solutions available today:

- Buildium: A property management software that handles diverse portfolios, including residential, commercial, and mixed-use properties.

- Landlord Studio: A property tracking software for monitoring financial data of rental properties.

- MaintainX: A maintenance management software that streamlines maintenance operations, tracks assets, and improves workflow efficiency.

- MyAssets: An all-in-one solution for organising property information, from associated finances to comprehensive records of each property’s contents.

- Rightmove: A property listing software that allows letting and estate agents to advertise properties for sale or rent.

Today's digital tools are indispensable for effective property management. By leveraging these platforms, both professional property managers and owners can streamline operations and oversee their portfolios from anywhere in the world.

Is it Worth Owning Property Abroad?

Buying overseas property can be highly rewarding, whether as a private getaway, an income-generating investment, or a future safety net. Still, it is a significant decision that requires careful thought due to the distinct challenges and factors involved.

While the lifestyle benefits and financial incentives are clear, success hinges on thorough preparation. From understanding local market drivers and foreign ownership restrictions to securing financing, a title deed, and considering tax implications, each of these factors is relevant when planning to buy a house overseas.

Digital tools, such as property management software, allow individuals to manage properties anywhere in the world. This technology securely stores vital records and documents, whether they are managing properties in Europe, Asia, or any other location, enabling efficient and organised operations regardless of distance.

Regardless of the complexities and length of the process, individuals can confidently navigate the purchase and management of international real estate by staying well-informed and utilising efficient resources.

Buying Overseas Property: Frequently Asked Questions

1. What is the easiest country to buy property in?

The easiest country in which to purchase property is subjective and largely dependent on an individual’s goals, though several destinations are highlighted. To name a few, countries such as Greece, Spain, Portugal and the United Arab Emirates provide streamlined Golden Visa programs, offering residency through real estate investment and easing the process for those seeking relocation or expanded visa-free travel opportunities.

2. What do you need to buy a property abroad?

To buy property abroad, an individual needs a significant budget, which should include a large deposit if financing is required, along with additional funds for taxes, legal fees, and currency exchange. It is also essential for them to thoroughly research the target country's property laws and market.

3. Can UK citizens get a mortgage for property abroad?

UK citizens can obtain a mortgage for overseas property, though this typically requires a specialist international arrangement. Options include securing financing through a UK lender with global operations, working with a local lender in the destination country, or releasing equity by remortgaging an existing UK property.

Your Global Property Portfolio, Organised with MyAssets

Are scattered property records slowing you down? For individuals who own a single property, the task is difficult enough, but for those with multiple properties or plans to acquire more, it only grows more complex without proper organisation. This is where MyAssets comes in, a property porfolio organiser that brings all records together to keeps property oversight streamlined and stress-free.

Aside from allowing real estate owners to upload property information, MyAssets as a comprehensive asset management solution allows management and tracking of other assets such as finances, collectables, and personal belongings in one platform.

MyAssets streamlines the tracking of physical assets with its smart asset linking feature. This powerful tool allows users to assign the location of their valuables—such as art, antiques, home appliances, and furniture—to a specific property, providing a clear and organised record of where all their collections and belongings are located.

It gets even better. MyAssets also features a document vault, a secure space where users can upload and store digital copies of vital documents, such as title deeds, contracts, and insurance policies. This ensures that all essential paperwork is safely organised and accessible whenever needed.

Ready to bring order to your portfolio? Organise everything with MyAssets free for 14 days.